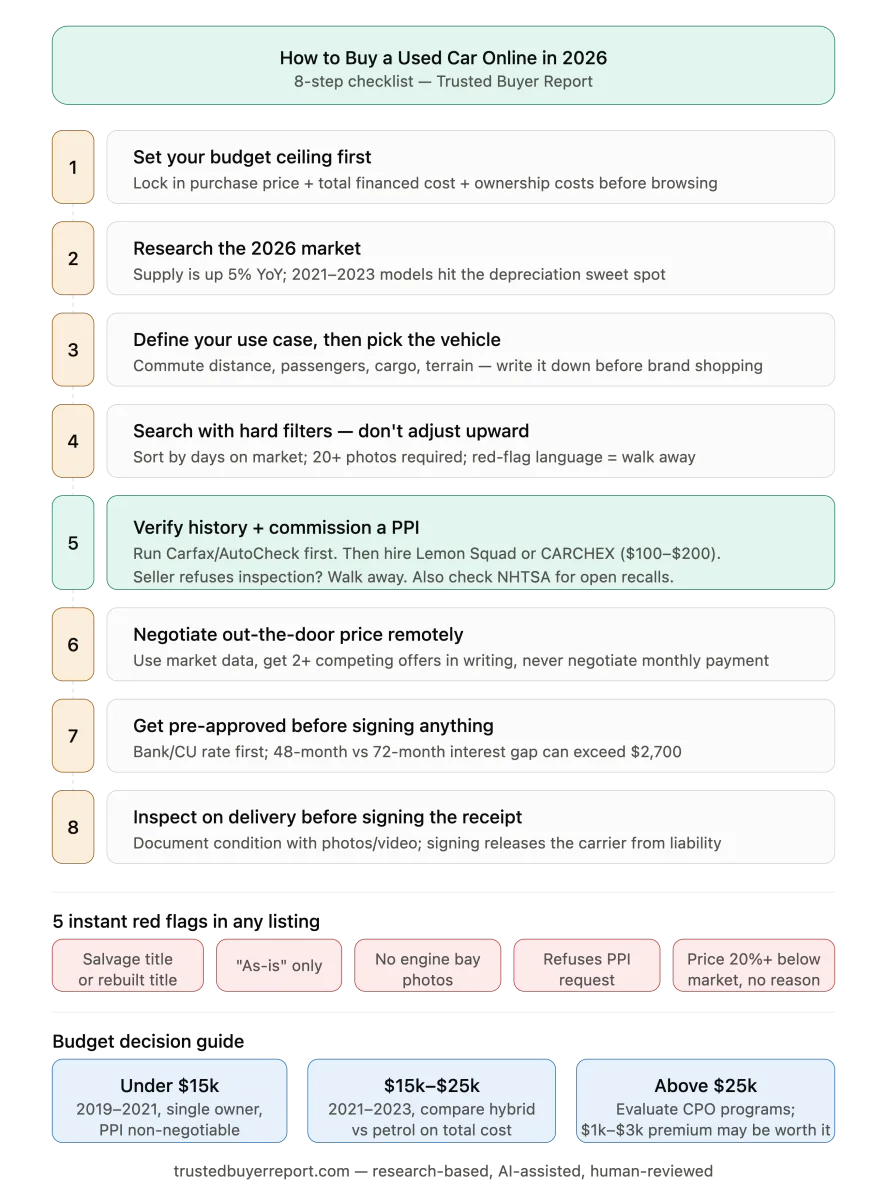

TL;DR — What this guide covers:

- How to set a real budget before you open a single listing

- Which model-year sweet spot gives the best value in 2026

- The two verifications that separate smart remote buyers from expensive mistakes

- How to negotiate out-the-door price from anywhere in the country

- What to check on delivery before the transport driver leaves

Most used-car guides start with platforms. This one doesn't.

The platform is the last thing that matters. What determines whether you close a good deal — or spend the next three years paying for someone else's accident — is the preparation you do before you ever contact a seller.

Here's the reality check: used vehicles are projected to capture 68.9% of the online car-buying market in 2026, according to Coherent Market Insights. The online used-car transaction is no longer an edge case — it's how most cars are bought. And yet 66% of buyers still want to physically experience a vehicle before purchasing, per Phyron's Car Buying Trends 2026. That tension — between the convenience of digital buying and the reality that cars break in ways photos can't show — is exactly what this guide is built to resolve.

Eight steps. No filler. Here's what actually matters.

Step 1: Set Your Budget Before You Open a Single Listing

The most common mistake online used-car buyers make is browsing before budgeting.

Once you see a vehicle you like, your brain works backward to justify the price. Set the ceiling first — then search.

Your budget has three distinct layers that most buyers conflate:

| Layer | What it covers |

|---|---|

| Purchase price | What you pay for the car itself |

| Total financed cost | Purchase price + interest over the loan term |

| Total cost of ownership | Loan + insurance + fuel + maintenance + repairs |

AAA's analysis via Jill on Money estimates total monthly vehicle ownership costs (new) at roughly $1,000/month. Used cars run lower, but the framework applies — your monthly exposure isn't just your loan payment.

Before you search, complete this sequence:

- Determine your maximum comfortable monthly payment, including insurance and fuel — not just the loan.

- Get pre-approved for an auto loan from your bank or credit union. This gives you a real rate and a firm borrowing ceiling.

- Decide how much you can put down. A larger down payment reduces loan balance and lowers the risk of being underwater on a depreciating asset.

- Add a buffer of $1,000–$1,500 for taxes, title, registration, and immediate maintenance.

Get the number locked before you fall in love with a listing.

Step 2: Understand the 2026 Used-Car Market Before You Search

Spending 30 minutes on market research is worth more than any negotiation tactic.

Here's where the market stands heading into mid-2026:

- Supply is up. According to Cox Automotive vAuto Live Market View data via Jupiter Chevrolet, nationwide used-vehicle inventory stood at 2.20 million units at the start of 2026 — a 5% year-over-year increase. Retail used-vehicle sales closed December 2025 at 1.34 million units, up 2.9% year over year. Buyers have more to choose from than a year ago.

- Wholesale prices are elevated but softening in select segments. The Manheim Used Vehicle Value Index was running roughly 4% above year-ago levels as of mid-May 2026. The spring bounce driven by tax-refund spending typically moderates in late summer — if you're not in a rush, waiting until August or September can mean better retail pricing in softening segments.

- Segment matters more than brand in 2026. CarEdge's 2026 used-car price forecast identifies trucks, hybrids, and SUVs as holding value well. Compact sedans and some first-generation EVs are softening — meaning more negotiating leverage if you're shopping those categories.

The model-year sweet spot in 2026? A 3-to-5-year-old vehicle — roughly 2021 to 2023 — gives you modern safety technology and current infotainment without absorbing the steepest portion of new-car depreciation. The original owner typically absorbed 30–40% of depreciation in the first three years. CarEdge describes this range as the best-of-both-worlds compromise for 2026 buyers.

Step 3: Choose the Right Vehicle Type for Your Actual Needs

Brand loyalty is expensive. Define your use case in concrete terms first.

Write down the answers to these before you search:

- Daily commute distance and whether it includes highway miles

- Number of regular passengers

- Cargo requirements (bikes, strollers, furniture, tools)

- Whether you tow anything, and if so, what

- Terrain you drive most often (urban, suburban, rural, mountain)

One of the underused advantages of online buying is geographic flexibility. Expanding your search radius to 200–300 miles — or even nationally — dramatically widens your options and increases your odds of finding a well-maintained example at a fair price.

Reliability data should drive your model-year shortlist, not marketing impressions. Consumer Reports uses a methodology that emphasizes value within a price range rather than headline scores — a meaningful distinction for used-car buyers.

A concrete example of why model year and trim matter together: the Toyota Highlander's 2017 model year made blind-spot monitoring and advanced safety features broadly available across trims, while the 2014–2016 versions required the top-trim Limited package for the same equipment. A 2016 LE and a 2017 XLE may both be within your budget — but they're meaningfully different vehicles for safety-conscious buyers.

Identify two or three acceptable alternatives before contacting any seller. If your only acceptable vehicle is a specific model in a specific color with specific options, you have no negotiating leverage and no fallback. Flexibility is a financial asset.

Step 4: Search Effectively Without Getting Overwhelmed

Set hard filters before you browse. Don't adjust them upward because a listing looks appealing.

Lock in your maximum price, mileage ceiling, model year floor, and transmission preference before you start. The moment you start making exceptions, you're letting the inventory dictate your criteria instead of your needs.

Sort results by days on market, not just price. A vehicle listed for 45–60 days may indicate hidden issues, or it may mean the seller is overpriced and motivated. Either way, that information is useful. A vehicle listed three days at a competitive price in a hot segment will move fast — act accordingly.

Read listing descriptions fully before clicking through photos. These phrases should disqualify a listing for most buyers without further investigation:

- "As-is"

- "Salvage title" or "rebuilt title"

- "Flood damage"

- "Structural damage disclosed"

These aren't bargaining chips for the average buyer. They signal risk that requires specialized knowledge to evaluate.

Photo count is a proxy for seller transparency. A thorough listing includes 20+ photos: all four exterior angles, the roof, undercarriage, engine bay, dashboard, all seat rows, cargo area, and close-ups of any existing damage. A listing with six exterior shots and nothing under the hood is hiding something — even if only the seller's indifference.

For any vehicle you're seriously considering, request a live video call or recorded video walkthrough before proceeding.

Cross-reference the VIN. In most listings, it's visible on the dashboard in photos. Note it, run it independently, and confirm it matches the listing. Takes two minutes and catches a surprising number of discrepancies.

Step 5: Verify Vehicle History and Condition Remotely

This is the step most guides gloss over. It's the one that separates good transactions from expensive regrets.

Start with a vehicle history report

Run the VIN through Carfax or AutoCheck. These services pull from insurance claims, DMV records, and auction data to reveal accident history, title issues, odometer discrepancies, number of previous owners, and available service records.

A clean report is necessary — but not sufficient. History reports only reflect what was reported to their data sources. An unreported fender repair at a cash body shop won't appear. A clean report clears the obvious red flags; it doesn't certify condition.

Commission a pre-purchase inspection (PPI)

This is non-negotiable. A PPI from an independent mechanic near the vehicle typically costs $100–$200 and gives you an objective assessment of mechanical condition, frame integrity, fluid health, tire wear, and deferred maintenance. A competent mechanic finds issues that no history report captures.

If a seller or dealer refuses an independent inspection — walk away. That refusal is the inspection result.

Finding a mechanic in a city you don't live in is straightforward. Two reliable options:

- Mobile inspection services like Lemon Squad and CARCHEX send certified technicians to the vehicle's location for a flat fee.

- AAA-approved repair shops: search for one in the vehicle's ZIP code and call directly. Most accommodate PPI appointments.

As CarEdge recommends, always request both a vehicle history report and a pre-purchase inspection before buying any used car.

Check for open recalls

Verify any open safety recalls yourself — for free — using the NHTSA VIN lookup tool at nhtsa.gov. It takes under two minutes and occasionally surfaces safety issues the seller is unaware of or hasn't disclosed.

Also ask the seller for:

- All available service records

- Any existing warranty documentation

- Confirmation that open recalls have been completed

Step 6: Negotiate the Price Remotely

Remote negotiation feels like a disadvantage. It usually isn't.

You have more time to think, more access to comparative data, and the psychological distance to walk away without the social pressure of a showroom. Use it.

Your negotiating foundation is market data, not emotion. Before making an offer, research what comparable vehicles — same model, year, trim, and mileage range — are actually selling for, not just listed for. Listing prices are aspirational; transaction prices are real.

Timing has real leverage. CarEdge's 2026 price forecast notes that late 2026 is a prime window for buyers in softening segments — particularly compact cars and some EVs — as dealers work to move inventory before wholesale auction values ease further.

Get competing offers in writing. Contact at least two other sellers with comparable inventory and document their offers. Then present them directly: "I have a written offer of $X from [Dealer B] for a comparable vehicle. Can you match or beat that?" This works as effectively over email as it does in person.

Always negotiate the out-the-door price — the total you pay including taxes, fees, and all dealer charges — not the monthly payment. A dealer can make almost any monthly payment work by extending the loan term. A 72-month loan at a higher rate on a depreciating asset is a worse deal than a 48-month loan at a lower rate, even if the monthly number looks smaller.

Once you reach an agreed price: get every term confirmed in writing via email before proceeding to paperwork. Verbal agreements in car sales are not agreements — they're starting points for the next conversation.

Step 7: Arrange Financing Before You Sign Anything

Dealer financing isn't inherently bad. Accepting it without comparison is how buyers routinely overpay by thousands.

Pre-approval from your bank or credit union before finalizing any deal gives you a benchmark rate and removes your dependence on whatever the finance manager offers.

The math on loan terms is stark. Consider a $20,000 loan:

| Term | Rate | Total Interest Paid |

|---|---|---|

| 48 months | 6% | ~$2,500 |

| 72 months | 8% | ~$5,200 |

Lower monthly payment, higher total cost. This is the most common financing trap in car buying.

For remote purchases specifically: confirm with your lender that they'll finance a vehicle purchased from an out-of-state dealer or private seller, and ask whether there are age or mileage restrictions on the vehicle. Some lenders won't finance vehicles older than a certain model year or above a certain mileage — discovering this after you've agreed on a price creates unnecessary complications.

Consider gap insurance on any financed used-car purchase. If the vehicle is totaled and you owe more than its current market value, standard auto insurance only pays the market value. Gap coverage pays the difference. It's typically inexpensive through your auto insurer — significantly more expensive when added through dealer financing.

Before signing: review the complete financing agreement and confirm the interest rate, loan term, total amount financed, and any add-on products. Extended warranties added to the financing agreement increase your loan balance and often cost more than comparable coverage purchased independently.

Step 8: Manage Delivery and Post-Purchase Protection

Once financing is arranged and paperwork signed, you need to manage the physical transfer.

For remote purchases, your main options are:

- Fly to the vehicle's location and drive it home

- Use a third-party auto shipping service

- Use the dealer's delivery service if offered

If the vehicle is being transported, do not cancel your current vehicle's insurance until the purchased vehicle is in your possession and inspected. Confirm with your insurer that the new vehicle is covered from the moment of purchase, not delivery.

On delivery: inspect the vehicle immediately and document its condition with photos and video before the transport driver leaves. Compare the condition to what was disclosed in the listing and the PPI report. If there is new transport damage, file a claim with the carrier before signing the delivery receipt — signing typically releases the carrier from liability.

Verify the warranty status. If the vehicle is still under the manufacturer's original warranty, confirm coverage transfers to you. If you purchased an extended warranty, understand exactly what it covers, what it excludes, and which repair facilities are authorized. A warranty that only covers repairs at dealers 500 miles away isn't useful for a daily driver.

Frequently Asked Questions

Is it safe to buy a used car entirely online without seeing it in person?

Yes — with the right verification steps. The key protections are a vehicle history report, an independent pre-purchase inspection by a mechanic at the vehicle's location, and a live video walkthrough. Skipping the PPI significantly increases your risk. The inspection is what makes a remote purchase as safe as an in-person one.

What is the best model year range for a used car in 2026?

A 3-to-5-year-old vehicle — roughly 2021 to 2023 — offers the best balance of modern features, reliability, and value. You avoid the steepest new-car depreciation while still getting current driver-assistance technology and infotainment systems. CarEdge describes this as the best-of-both-worlds range for 2026 buyers.

How do I find a mechanic to inspect a car in a city I don't live in?

National mobile inspection services like Lemon Squad and CARCHEX send certified technicians to the vehicle's location for a flat fee. Alternatively, search for AAA-approved repair shops in the vehicle's ZIP code and call directly — most perform pre-purchase inspections in the $100–$200 range.

Should I use dealer financing or get pre-approved first?

Always get pre-approved from your bank or credit union before finalizing any deal. This gives you a benchmark rate and negotiating leverage. Dealer financing can occasionally be competitive — manufacturers sometimes offer promotional rates on certified pre-owned vehicles — but you can't evaluate whether it's a good deal without a comparison figure in hand.

What are the biggest red flags in an online used-car listing?

Salvage or rebuilt title disclosure, "as-is" language without explanation, fewer than ten photos with no engine bay or undercarriage shots, a VIN that doesn't match across photos, a seller who refuses an independent inspection, and a price significantly below market comparables with no explanation. Any one of these warrants caution. Multiple red flags in a single listing should end your interest.

Is 2026 a good time to buy a used car?

Supply is up 5% year over year, giving buyers more options than in recent years. Compact cars and some EVs are softening — creating negotiating room in those segments. Trucks, SUVs, and hybrids are holding value, meaning less pricing leverage for buyers in those categories. If your target vehicle is in a softening segment, waiting until late summer or fall 2026 may yield better pricing as wholesale values ease through to retail.

Decision Framework: Which Budget, Which Strategy

The online used-car market in 2026 rewards preparation and penalizes impatience. Here's a concrete framework based on budget:

Budget under $15,000: Focus on the 2019–2021 model year range in reliable mainstream brands. Prioritize single-owner vehicles with documented service history. A PPI is non-negotiable at this price point — repair costs represent a larger percentage of the vehicle's value. Mechanical issues that would be minor on a $25,000 car are budget-breaking on a $12,000 one.

Budget $15,000–$25,000: Target the 2021–2023 range. You can access modern driver-assistance features without paying new-car prices. Compare hybrids against petrol equivalents — in this range, the hybrid premium on a used vehicle is often modest and the fuel savings are meaningful over a 3-5 year ownership period.

Budget above $25,000: Certified pre-owned (CPO) programs are worth evaluating seriously. CPO vehicles come with manufacturer-backed extended warranties, multi-point inspection records, and in some cases promotional financing rates. The CPO premium is real — typically $1,000–$3,000 above a comparable non-certified vehicle — but the warranty and inspection documentation can justify it for buyers who want reduced risk.

How this guide was researched: This guide is based on publicly available market data from Cox Automotive, Manheim, Coherent Market Insights, CarEdge, and the NHTSA, combined with expert analysis from Consumer Reports and verified automotive buying research. Trusted Buyer Report has not independently tested or purchased the vehicles referenced. Sources are cited throughout.

This article was drafted with AI assistance and fact-checked by a human editor before publishing. Read our editorial standards →